You’ve probably heard someone use the term “equity” or “equity event” when talking about a home loan, commercial loan, or a number of other loans. But what is an equity event in commercial real estate and how exactly does it affect your deal? During an equity event, a person or company either (1) refinances the loan, most commonly to pull out accrued equity or (2) places an additional/supplemental loan on the property at the same or more favorable terms, also for the purpose of pulling out built up equity. In terms of how an equity event affects your deal and more specifically your or your investors CoC (cash-on-cash), see the chart below:

Makes complete and total sense, right? Cool, email me with any questions!

I kid, I kid… let’s break this down. But first, we need to simplify some things and make some very basic assumptions in order to make this as easy to follow as possible. I’ll use a made up example from a fairly common syndication structure (Note: Keep in mind that in an actual real estate deal, there are a lot more factors that influence your or your investor’s bottom dollar. Additionally, return metrics for syndicated commercial real estate deals will vary widely based on a number of factors, so metrics used here should not be considered standard or universal.)

Assumptions:

- No attrition* (Note: Attrition refers to a decrease in ownership share proportional to your decrease in invested equity during a refinance and return of capital. I.e. if you invest $100K at an 8% pref, and $50K was returned during an equity event, your 8% pref would now be based on $50K, not your initial investment of $100K. Whether or not there is attrition depends on the Sponsor and how they structure their deals, be sure to ask questions to find these types of details out)

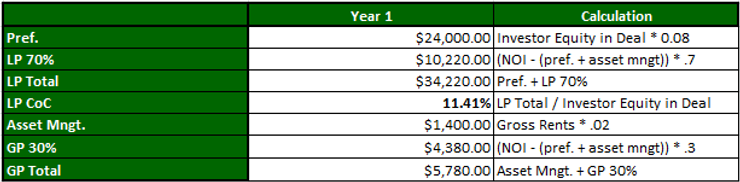

- 8% preferred return (pref) to the LP (limited partners/investors) and 2% asset management fee to the GP (general partner/Sponsor)

- 70/30 split thereafter

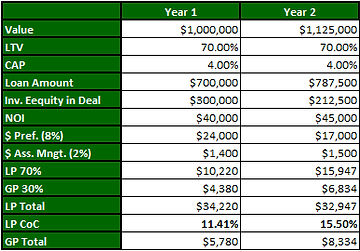

- $1MM initial property value

- 70% LTV (loan-to-value)

- 4% CAP (steady)

- 4.25% interest

- 2 year interest only loan

- Year 1 = standard operations, $40K NOI (net operating income), $70K gross rents

- Year 2 = refinance at the beginning of the year, $45K NOI, $80K gross rents

- We will let let NOI account for interest/loan payments, which is typically not the case in a standard pro-forma

- To stress again, an actual real estate deal is not this simple. A much broader scope of factors need to be considered when calculating performance. I’ve made this a simple, high-level overview of how an equity event can affect your CoC returns.

Year 1

So we’ve bought a property valued at $1MM at a LTV of 70% and a CAP of 4%. The LTV is simply your total loan amount as a percentage of the property value, which means that our loan amount is $700K and that we’ve raised $300K from investors to make up the difference. So, with an NOI of $40K (this is one of our assumptions, but can also be calculated using CAP*value), our returns look as follows:

Year 2

We’re now in year two and we’ve been working diligently to increase income and decrease expenses, thus driving NOI from $40K to $45K. Naturally, we decide to take advantage of this increase in property value (since increase NOI drives value) and refinance the property (the equity event) in order to pull out equity and return it to investors. Since the property is now valued at $1.125MM ($45,000/.04) and our original $700K loan puts us at a new LTV of 62%, we can refinance to get us back up to the original 70%. At an LTV of 70% of the new value, our new loan is equal to $787,500, which we use to pay off the original loan and return the rest to investors. Here’s how that looks from $40K NOI to our increased $45K NOI:

Now, let’s take a look at our new returns, taking in to account the new NOI, the new investor equity in the deal and the additional interest payment we’ve now incurred due to the higher loan amount (Note: This assumes that the interest rate has remained the same, which I’ve done for?… you guessed it… simplicity)

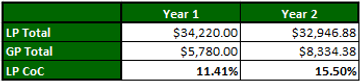

As you can see, our investor CoC has increased considerably. Let’s look at our most important return values side by side to fully grasp the effect of this equity event:

In summary, the GP is incentivized by a refinance as their total take increases. Some may see the decrease in total annualized dollars for the LP and think of it as a bad thing, but those people should keep in mind the following crucial facts:

- Your CoC (a key metric when considering the success of an investment) has increased; your dollars are now working harder for you.

- An equity event such as this will allow you to increase your ownership basis at no additional cost. Example: you bought into the above deal at $300,000, a refinance returned $87,500 but your ownership in the deal is still based on your initial $300,000 investment. Now, you can take those 87,500 tax free dollars* (Note: The IRS classifies the return of investor equity as a non-taxable event.) and invest them into another syndicated deal, the stock market, different real estate niches, whatever your heart desires; this results in $387,500 worth of ownership for the price of $300,000. This point, to me, is one of the most wildly powerful concepts/tools in all of real estate investing.

That wraps up Installment 1 of the Syndication Return Metrics Series. What are your thoughts? Have you had similar or different experiences when refinancing a property? Are you a passive investor considering partnering with a Sponsor and found this to be beneficial? Are you a GP/underwriter and believe I left something out? I’d love to hear your thoughts on this simplified equity event example, so let’s discuss in the comments below!!